Refinancing your FHA loan in Fullerton does not have to be the complex, paperwork-heavy ordeal that many homeowners expect. The Fprogram was designed specifically to make the process faster, simpler, and less invasive than a standard refinance. If you currently have an FHA loan, this option could put meaningful savings back into your monthly budget with far less friction than you might expect.

Many Fullerton homeowners stay in higher-rate FHA loans long after better options become available simply because they assume refinancing means starting the entire mortgage process from scratch. The Streamline program eliminates most of the hurdles that create that hesitation. Understanding how it works could be the first step toward a lower monthly payment and improved long-term financial health.

What Is the FHA Streamline Refinance Program?

The FHA Streamline Refinance is a simplified refinancing option available exclusively to homeowners who already have an existing FHA-insured mortgage. The program reduces the documentation requirements significantly compared to a traditional refinance, which is where the term “streamline” comes from. No full home appraisal is typically required, and income verification requirements are much lighter than standard loan processes.

To qualify, your existing loan must be in good standing, meaning your payment history reflects responsible management over recent months. The refinance must also produce a clear financial benefit for you, which typically means a lower interest rate or reduced monthly payment. Your loan program options and specific terms depend on your current loan details and the current market rate environment.

Key Benefits of Streamlining Your FHA Loan in Fullerton

The primary appeal of this program is the speed and simplicity it offers compared to conventional refinancing routes. Because the FHA already insures your current loan, the lender does not need to re-verify everything from scratch. This means less time waiting, fewer documents to gather, and a smoother experience from application to closing.

Fullerton homeowners who refinanced into FHA loans when rates were higher now have an opportunity to capture lower monthly costs without the typical barriers. The reduction in your interest rate directly translates into savings that compound over the remaining life of your loan. Even a modest rate reduction on a substantial loan balance produces meaningful savings when projected over five to ten years.

No Appraisal Required in Most Cases

One of the biggest advantages of the Streamline program is that the FHA typically does not require a new home appraisal. This matters particularly in markets where property values have fluctuated, as it removes the risk of an appraisal coming in lower than expected and derailing your refinance. Your loan is evaluated based on the original appraised value, which protects you from current market volatility.

Skipping the appraisal also removes one of the most common delays in the refinancing process. Traditional refinances can get stuck waiting for appraisal scheduling, completion, and review. The Streamline program bypasses this entirely in most qualifying scenarios, keeping your timeline tight and predictable.

Reduced Documentation Requirements

Unlike a traditional refinance that demands full income verification, employment documentation, and comprehensive asset statements, the Streamline program takes a lighter approach. Your lender will still review your payment history and confirm your existing loan details, but the process does not feel like applying for a brand new mortgage. This is a significant relief for self-employed borrowers or anyone whose income documentation is complex.

The reduced paperwork also means fewer opportunities for the process to stall while you track down additional documentation. Most borrowers find the experience notably less stressful than their original purchase loan application. The mortgage process is designed to be clear and efficient from start to finish.

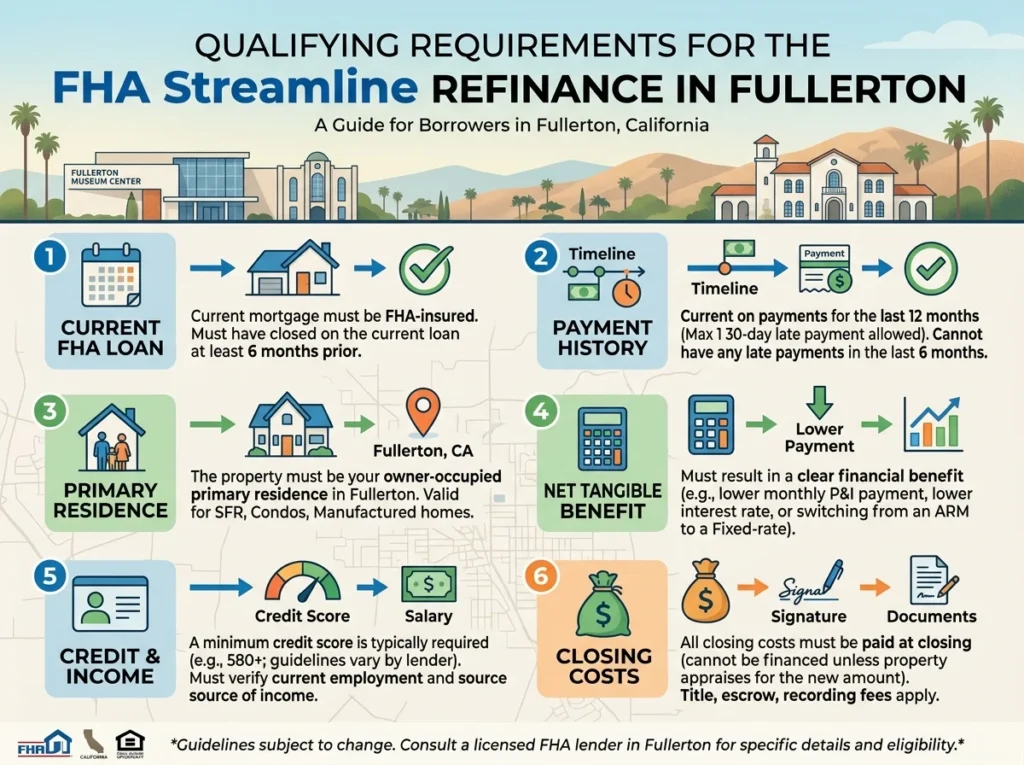

Qualifying Requirements for the FHA Streamline in Fullerton

While the process is simplified, there are still specific criteria your loan must meet before you can proceed. Your existing FHA loan must have been open for at least 210 days before you can apply for a Streamline Refinance. You must also show that you have made at least six on-time payments on your current loan during that period.

The net tangible benefit rule is another critical requirement your new loan must genuinely improve your financial position in a measurable way. This typically means a reduction in your combined interest rate and mortgage insurance premium of at least half a percent. Lenders will calculate this figure for you and confirm whether your situation meets the threshold before moving forward.

Credit Score Considerations

While the Streamline program does not impose the same strict credit review as a full refinance, most lenders still have minimum credit score overlays they apply. A score of 580 or better is generally sufficient for most participating lenders, though some may have slightly higher internal requirements. Reviewing your credit before applying ensures there are no surprises during the process.

If your score has improved since you originally took out your FHA loan, you may qualify for better terms than you originally received. A higher credit score often translates to better pricing even within the Streamline framework. It is worth reviewing your full credit picture before starting the application.

Closing Costs on a Streamline Refinance

Every refinance involves some level of closing costs, and the FHA Streamline is no different. The good news is that costs associated with this program are generally lower than a full refinance because fewer services are required. Typical costs include lender fees, title insurance update charges, prepaid interest, and government recording fees.

You have options when it comes to covering these costs. Some borrowers choose a no-closing-cost structure where the fees are rolled into a slightly higher interest rate, eliminating the need to bring cash to the table. Others prefer paying costs upfront to secure the lowest possible rate. Your competitive rates and fees conversation with your lender should cover both approaches so you can choose what fits your goals.

How Much Can Fullerton Homeowners Save?

The actual savings depend on the gap between your current rate and today’s available rates, as well as your remaining loan balance. Even a reduction of 0.5% to 1% on a $450,000 loan balance produces several hundred dollars in monthly savings. Projected over five years, that figure becomes a very compelling reason to move forward.

Use our mortgage rate calculator or speak directly with a Southern California mortgage expert to run actual numbers based on your specific loan. Seeing your projected savings in writing makes the decision much clearer. Most homeowners who qualify find that the break-even point on their closing costs arrives well within the first two years.

Is a lower monthly payment possible for your Fullerton home? Reach out to Nathan Carpenter today and find out if you qualify for a fast, easy FHA Streamline Refinance.

Frequently Asked Questions

How long does an FHA Streamline Refinance take to close?

Because the documentation requirements are reduced and no appraisal is typically needed, most Streamline Refinances close within 20 to 30 days. Working with an organized lender who communicates clearly keeps the timeline on track from application through funding.

Can I take cash out with an FHA Streamline Refinance?

No the Streamline Refinance is designed solely to improve your rate and payment, not to access your equity. If you want to pull cash from your home, a standard FHA cash-out refinance is the appropriate product for that goal.

Does my home need to pass an inspection for the Streamline program?

Generally no formal inspection is required as part of the FHA Streamline Refinance process. The program focuses on your payment history and financial benefit rather than re-evaluating your property’s physical condition.