Owning investment properties in Orange County feels exciting until the bank says no. You have high rental income on paper, yet your personal debt-to-income ratio blocks the deal. Many investors hit this wall when they try to grow their portfolios.

DSCR loans change the game for real estate investors here in Southern California. Understanding how these fit within comprehensive mortgage financing options helps you build a complete investment strategy. These loans focus on what the property can earn instead of your W-2 or tax returns. If you want to scale faster in areas like Irvine, Laguna Niguel, or Newport Beach, understanding DSCR loan California options can open doors that conventional financing keeps shut.

What Is a DSCR Loan?

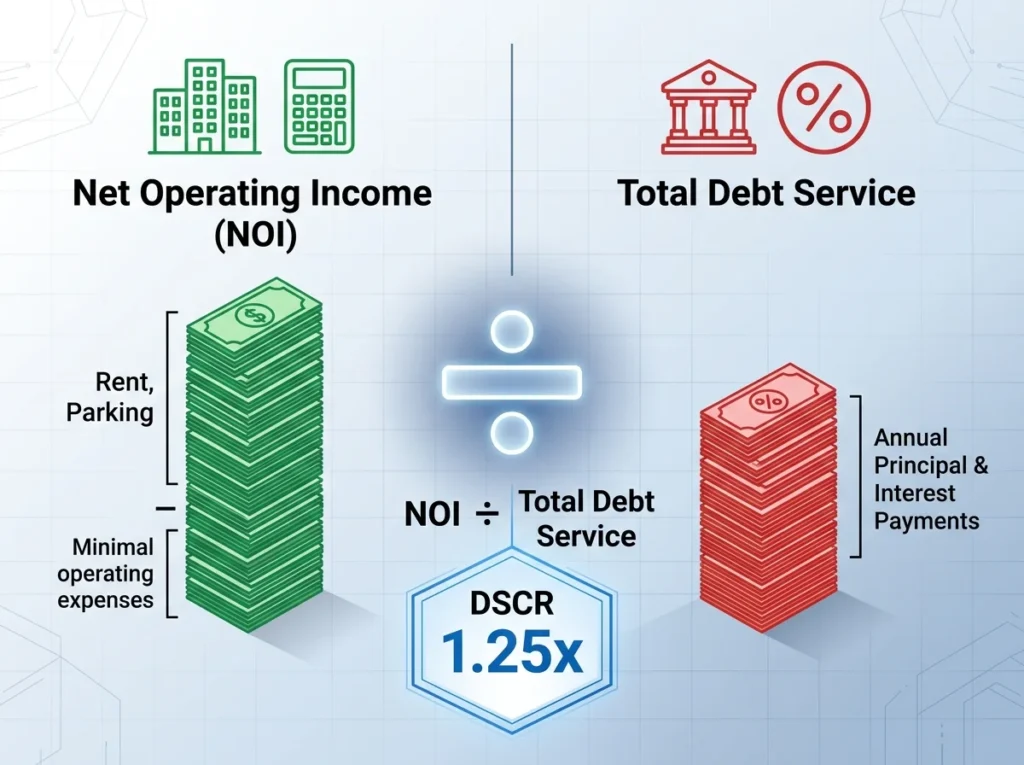

A DSCR loan stands for Debt Service Coverage Ratio loan. Lenders look at the property’s rental income to decide if it can cover the mortgage payment. They calculate the ratio by dividing the monthly rent by the total housing payment, which includes principal, interest, taxes, insurance, and any HOA fees.

This approach works especially well for investors who own multiple properties or rely on rental cash flow. You do not need to show personal income verification like on a traditional loan. Many self-employed investors and real estate portfolio owners in Orange County prefer this route because it simplifies the process.

In short, the property has to pay for itself. A solid DSCR ratio shows lenders the investment makes financial sense on its own.

DSCR Loan Requirements in Orange County, CA

DSCR loan requirements focus more on the asset than on you. Lenders typically want a minimum credit score of around 640, though 700+ helps you secure better terms. Most programs ask for a down payment of 20-25 percent, but this can vary.

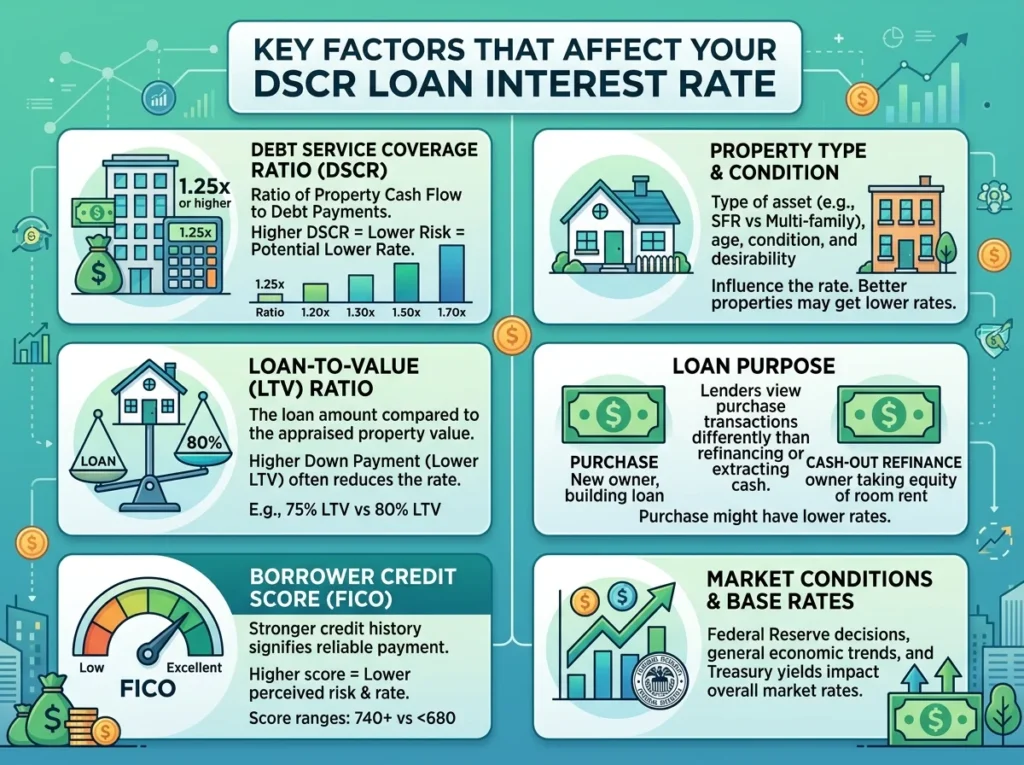

The key number is your debt service coverage ratio. Many lenders look for 1.0 or higher, meaning the rent covers the full mortgage payment. Stronger ratios above 1.25 often unlock lower DSCR loan interest rates and more favorable conditions.

Other common requirements include a property appraisal and proof of the expected rental income. For short-term rental financing like Airbnb properties in tourist-friendly Orange County spots, lenders may use market data or booking history to verify income.

How the Debt Service Coverage Ratio Calculation Works

The calculation is straightforward. Take the monthly rental income and divide it by the proposed monthly mortgage payment (PITIA). For example, if a property rents for $5,000 and the total payment equals $4,000, your DSCR equals 1.25.

Lenders run investment property cash flow analysis during underwriting. They review comps, local market rents, and operating expenses. This rental income verification process helps them feel confident in the loan.

Higher ratios signal lower risk. They often lead to better DSCR loan interest rate offers and higher loan-to-value ratio approval.

DSCR vs Conventional Loan: Which Fits You Better?

Many investors compare DSCR vs conventional loan options before deciding. Conventional loans dig deep into your personal income, employment history, and overall debt load. They work great if you have a steady W-2 income and low existing debt.

DSCR loans skip most of that personal scrutiny. They shine when you want to grow a real estate portfolio loan without hitting debt-to-income walls. You can often finance more properties because each one stands on its own cash flow merits.

The tradeoff usually comes in slightly higher interest rates. However, the speed, flexibility, and ability to qualify without income docs make DSCR loans worth it for many Orange County investors chasing short-term rental financing or long-term holds.

Benefits for Orange County Real Estate Investors

Orange County’s strong rental demand and tourism make DSCR loans especially powerful. Many sophisticated investors combine DSCR loans with jumbo loans for high-value property acquisitions to maximize their Orange County portfolio. You can move quickly on properties in competitive neighborhoods without waiting for personal income paperwork.

These loans support both traditional long-term rentals and short-term rental financing strategies. Many programs accept projected Airbnb income with proper documentation. This flexibility helps investors maximize returns in high-demand areas.

You also gain scalability. Unlike conventional limits on financed properties, DSCR underwriting guidelines let you build a larger portfolio based on strong asset performance rather than your personal financial picture.

Key Factors That Affect Your DSCR Loan Interest Rate

DSCR loan interest rates depend on several elements. Your credit score, the property’s DSCR ratio, down payment size, and overall loan-to-value ratio assessment all play roles. Stronger numbers across the board bring better pricing.

Current market conditions influence rates, too. Shop around with experienced lenders who understand investment property loan structuring in California. A small difference in rate can have a big impact on your monthly cash flow and long-term returns.

Experienced mortgage professionals can help you model different scenarios and find the sweet spot for your goals.

Common Challenges and How to Overcome Them

Some investors worry about higher rates or stricter property standards. The solution starts with preparation. Run your own cash flow numbers before you shop. Understand local rents and expenses in your target Orange County neighborhood.

Work with a lender who specializes in DSCR loans and knows the Southern California market. They can guide you on the best ways to strengthen your application through rental income documentation or strategic down payment choices.

Ready to Grow Your Orange County Investment Portfolio?

DSCR loans give serious real estate investors the financing tool they need to move faster and scale smarter in a competitive market. Whether you are adding your first rental or expanding an existing portfolio, the right structure makes all the difference.

At Nathan Carpenter Loans, we help Southern California investors navigate DSCR loan requirements and find solutions that fit their unique situation. With transparent communication and a simple process, we make investment property financing straightforward.

Discover your DSCR loan options today with Nathan Carpenter’s investment property expertise. Call or reach out through the website to schedule a no-pressure conversation about maximizing your investment potential. Let’s explore how these powerful financing tools can work for your portfolio.

FAQs About DSCR Loans in Orange County

What is a DSCR loan?

A DSCR loan qualifies you based on the rental income the property generates rather than your personal income or tax returns. It focuses on the debt service coverage ratio to ensure the investment can cover its own mortgage.

What are typical DSCR loan requirements in California?

Lenders usually want a minimum DSCR of 1.0 or higher, a credit score around 640+, and a 20-25% down payment. Exact terms depend on the property and your financial profile.

How does a DSCR loan compare to a conventional loan?

DSCR loans ignore your personal debt-to-income ratio and focus on property cash flow. Conventional loans require strong personal income documentation and can limit portfolio growth.

Can DSCR loans work for short-term rentals?

Yes. Many programs support short-term rental financing using market data or booking history to verify income potential, which is great for Orange County vacation areas.

Will my DSCR loan interest rate be higher?

Rates are often slightly higher than conventional loans, but strong property performance and credit can help you secure competitive terms. An experienced lender can shop for the best options for you.