Huntington Beach offers that perfect mix of beach life, good schools, and easy access to Orange County jobs. Yet many buyers hit a wall when they start looking at homes. Prices often push well past the point where standard loans work. You find the right property near the surf, only to realize the financing feels complicated.

This challenge hits especially hard with luxury or larger homes. Orange County home prices keep many dream homes just out of reach without the right loan. A jumbo mortgage California can open doors, but only if you understand how these loans differ from everyday options. Nathan Carpenter helps local Huntington Beach buyers cut through the confusion every day with expert guidance and transparent communication

Why Huntington Beach Demands Jumbo Loan Thinking

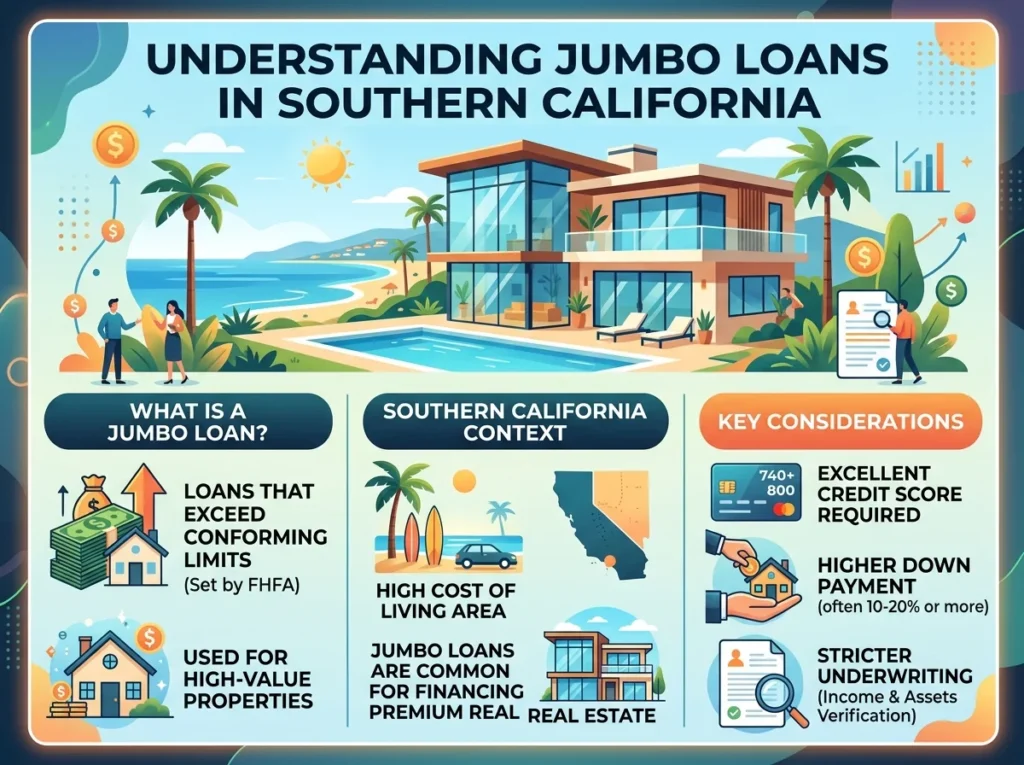

Homes here sell fast in a competitive market. Many listings sit above $1.3 million, and ocean-close properties climb higher. The 2026 high-balance conforming limit in Orange County tops out around $1,249,125 for single-family homes. Anything bigger falls into jumbo territory.

Buyers often need expensive home financing options that match these price tags. Standard loans stop working once you cross that threshold. Jumbo programs step in, but they come with their own set of rules around reserves, income, and credit. Understanding these early saves time and stress. For qualifying military veterans, VA loans offer powerful zero down payment alternatives – though many Huntington Beach properties exceed VA limits, making jumbo financing the practical choice for luxury and higher-priced coastal homes in this competitive market.

Many families arrive ready to buy a luxury home only to discover appraisal gaps or stricter underwriting. Local knowledge makes all the difference. Nathan Carpenter knows the Huntington Beach market and pairs it with strong lender relationships.

Understanding Jumbo Loans in Southern California

A jumbo loan Huntington Beach simply means a mortgage larger than what government-backed limits allow. These loans let you finance higher-value properties without splitting the deal into multiple loans.

Lenders review these files manually. They look closer at your full financial picture. This process protects everyone, but it requires solid preparation from you as the buyer.

Jumbo mortgage California options vary by lender. Some focus on low rates while others offer more flexible terms. Shopping around pays off, especially when rates and reserve needs differ.

Key Jumbo Loan Challenges in Huntington Beach

Strict Qualification Standards

Jumbo loans usually need stronger credit scores and lower debt loads. Lenders often want a credit score in the mid-700s or higher for the best terms. Your debt-to-income ratio analysis becomes critical here.

Most programs prefer a DTI under 43%. Some go lower for bigger loans. This keeps your monthly payments manageable even with larger balances.

Jumbo loan income requirements also rise. Lenders verify steady, documented earnings over two years. Self-employed buyers need extra paperwork, but solid tax returns and reserves often help with approval.

Cash Reserve Needs

Jumbo loan cash reserves stand out as one of the biggest differences. Many lenders want six to twelve months of mortgage payments set aside after closing. This buffer shows you can handle payments if life throws a curveball.

These reserves sit in addition to your down payment and closing costs. Liquid assets, retirement accounts, and investments often count toward this total. Planning ahead makes this requirement easier to meet.

Loan-to-Value and Appraisal Considerations

Loan-to-value (LTV) assessment plays a big role. Many jumbo programs work best with 20% down or more, though some go as low as 10% for strong borrowers. Lower LTV means less risk for the lender and often better rates for you.

Appraisals matter more for higher-end homes. Appraisal gap risk evaluation helps you prepare. In a hot area like Huntington Beach, strong comparable sales support values, but having extra cash ready covers any surprises.

Smart Strategies for Jumbo Loan Success

Prepare Your Documentation Early

Jumbo loan application tips start with organization. Gather two years of tax returns, W-2s, pay stubs, and bank statements. Self-employed borrowers should prepare profit-and-loss statements too.

Strong pre-approval documentation sets you apart in competitive offers. Sellers notice when buyers arrive with full approval letters instead of simple pre-qualifications.

Compare Rates and Lenders

Interest rate comparison deserves your attention. Jumbo rates sometimes run slightly higher than conforming loans, but they change daily. Working with an experienced broker like Nathan Carpenter gives access to multiple lenders and better choices.

Some programs reward larger down payments or extra reserves with improved pricing. When you review all available loan programs, you’ll see how jumbo loans compare against conventional, VA, and FHA options – Nathan helps Huntington Beach buyers understand every financing path so you choose the solution that truly fits your financial goals and timeline. Others focus on speed or flexible income sources.

Build a Luxury Home Financing Strategy

Think beyond the basic loan. A good luxury home financing strategy considers your full financial life. This includes future plans, investment properties, and cash flow.

Nathan Carpenter reviews your whole situation. He helps match the right product to your goals instead of pushing one-size-fits-all options.

Overcoming Common Jumbo Loan Hurdles

Buyers sometimes worry about stricter rules. Yet many qualified families close successfully with the right guidance. Clear communication during underwriting keeps things moving.

Home loan Huntington Beach buyers benefit from local expertise. Nathan knows which appraisers understand the area and which lenders close jumbo files quickly here.

Reserve requirements feel tough, but creative solutions exist. Some programs accept gifted funds or retirement assets under certain conditions. Others offer portfolio loans with different guidelines.

Huntington Beach’s competitive market demands a financing partner who understands jumbo loan challenges and has real solutions. Don’t let underwriting complications stop your dream. Explore jumbo loan solutions with Nathan Carpenter today – schedule your no-pressure consultation to discuss your Huntington Beach home goals, understand your options, and discover how to navigate the path to homeownership with confidence and clarity

Jumbo Loan FAQ

What credit score do I need for a jumbo mortgage in California?

Most lenders look for 700 or higher. Scores in the mid-700s usually unlock better rates and terms. Stronger credit also helps with reserve and DTI flexibility.

How much cash reserves should I expect for a jumbo loan?

Six to twelve months of payments is common. Exact needs depend on your loan size, credit, and the specific lender. Nathan reviews options that match your situation.

Can I buy a home in Huntington Beach with less than 20% down using a jumbo loan?

Yes, in many cases. Some programs allow 10–15% down for well-qualified buyers. Your overall financial strength determines what is possible.

What makes jumbo underwriting different from standard loans?

Lenders manually review every file. They pay close attention to jumbo loan underwriting guidelines, reserves, and property details. This extra step protects both sides but needs good preparation.

Are jumbo loans harder to get approved right now?

They require more documentation than smaller loans. Yet buyers with solid income, credit, and reserves succeed regularly. Local experience helps navigate the process smoothly.

Ready to explore your jumbo loan solutions in Huntington Beach?

Nathan Carpenter offers clear, transparent communication and a simple mortgage process. Whether you need help with jumbo loan challenges, pre-approval, or comparing options, his team makes it straightforward.

Contact Nathan Carpenter today to schedule a no-pressure conversation about your Huntington Beach home goals. Let’s find the right financing path together and get you into the coastal home you want.